Index Coop (INDEX) Analysis

On-Chain Passive Indices

Background

As cryptocurrencies grow in popularity, the infrastructure to support large scale investing needs to be developed. One of the key investment tools is index products. Crypto investing differs from traditional markets in several key elements, and one of the main ones is the increased risk of permanent loss of capital.

Digital assets and tokens are much easier to launch at an earlier stage than traditional equities, so the average cryptocurrency tends to more closely resemble a liquid VC bet rather than a stock. Given the high risk of permanent capital loss, the efficient number of holdings to diversify away from idiosyncratic risk is much higher in crypto than in traditional markets. Furthermore, there are no standard reporting procedures for tokens and the technology behind many of these tokens is difficult to understand.

While the complexity of the crypto space makes it a difficult asset class for non-crypto natives to invest in, Index products make investing in crypto much easier because they give access to thematic and sector indices managed by investment experts in the space.

Despite the clear need for crypto index products, index products are still early in their market penetration of the overall digital asset space. Roughly 17% of the global equities market is structured through index products. Currently index products represent less than 5% of all digital assets and most of that exists in Grayscale products.

Traditional market crypto index funds like Grayscale Defi Fund serve a fundamentally different clientele than on-chain indices. The Defi Pulse Index can be used for collateral on Aave and requires custodial solutions. Grayscale funds require a brokerage account. In the long run these two different products may start to compete, but for now they appeal to different customer bases.

Index Coop

Index Coop is a DAO built on Set protocol that enables the creation of crypto indices.

Index currently offers 6 index products: Defi Pulse Index, Metaverse Index, ETH 2X Leverage Index, BTC 2X Leverage Index, DATA Economy Index, and BED Index.

● Defi Pulse Index is the largest on-chain defi index by AUM. It’s a market cap weighted index that tracks the top defi projects offered on the Ethereum blockchain.

● Metaverse Index is the largest on-chain NFT/metaverse index by AUM. It’s designed “to capture the trend of entertainment, sports, and business shifting to take place in virtual environments”. It weighs its holdings based on liquidity and market cap.

● BTC & ETH 2X Leveraged Indices offer easy access for DEX users to get access to leverage on BTC and ETH.

● Data Economy Index: is a data centric and chain agnostic index. It includes tokens from any blockchain that provide data-based products or services

● The BED Index is an equal weight index of the Defi Pulse Index, Bitcoin, and Ethereum. It aims to give safe, passive exposure to the upside of crypto.

There are also several additional products that are in the pipeline.

Monetary Policy / Tokenomics

The Index Coop charges streaming fees on these indices as well as burning and minting fees. streaming fees are an annual management fee that accrues linearly. The streaming fees are accrued each block and are based on TVL at the time. Minting/burning mechanisms allow arbitrageurs to sell the underlying holdings of the fund to keep the price of the index aligned with its underlying holdings. These arbitrageurs are charged a fee on their earnings.

Operating Metrics / KPIs

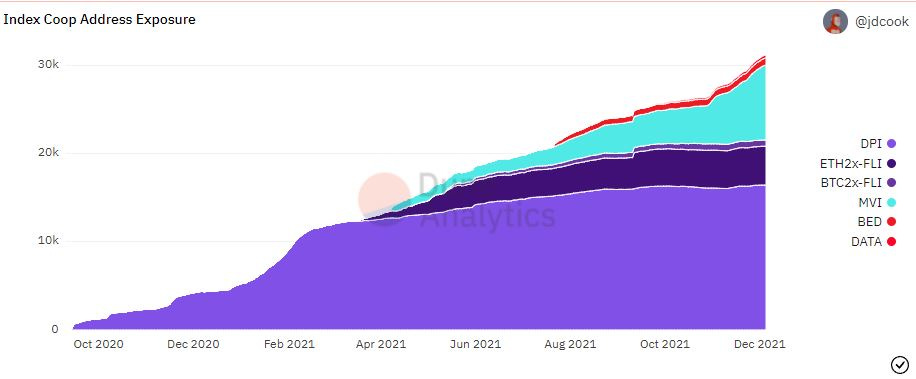

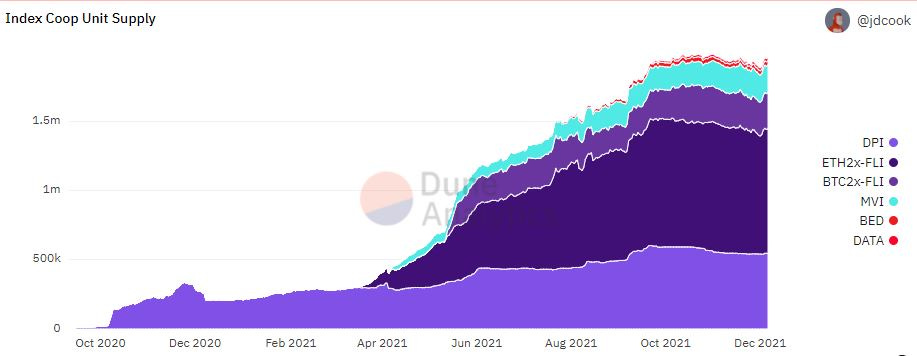

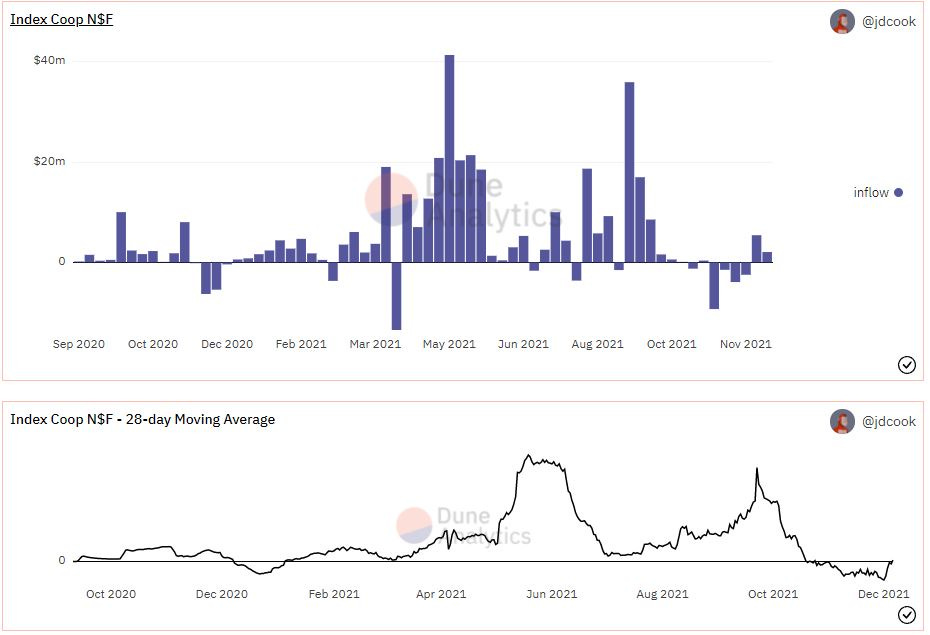

Index Coop measures its progress using its north stars. Community members work directly to increase address exposure, product unit supply, and product exposure across the crypto ecosystem.

Although there’s consistent growth in address exposure, there’s also net outflows from the index products.

The outflows are coming from all the index products. A large contributor to outflows is Indexed Finance (a direct competitor) getting exploited. Investors in on-chain passive indices likely noticed the devastation of a direct competitor being exploited and decided to reduce risk.

Competitive Analysis

There are several on-chain index protocols. These protocols range in design, but generally are either using Token Sets, Balancer pools, or are using some other synthetic or asset backed mechanism.

Currently there aren’t any competitors that have gained similar traction to Index Coop’s products. Ultimately the #1 on chain sector indices will have a large amount of the market share because of their network effects. On-chain indices need to be integrated into other defi protocols to provide competitive advantages over traditional crypto indices. On-chain indices that get sufficiently large will be the first integrated into other defi protocols. Defi Pulse Index is the first one to be added into Aave V2. It was able to do this because it was large enough and liquid enough to meet Aave’s requirements.

This flywheel of growing TVL leading to increased liquidity and defi protocol acceptance is key to why the on-chain index market is likely a “winner take most” market.

Future Plans

Currently, Index Coop is focused on expanding its customer base to include institutions, launching additional index products, improving capital efficiency, and finding new revenue generating activities.

One of the tools for increasing capital efficiency is lowering liquidity mining. Since November 2020, incentivized supply has dropped from over 80% to 0%.

Earlier in July, it raised $7.75 million for its treasury from Galaxy Digital, Wintermute, Defiance, 1kx, and others. Besides diversifying the Index treasury into dollars to fund operations, this raise also helped bring on investors with institutional connections that could help facilitate the coop's institutional customer acquisition strategy.

Besides the 4 index products currently available, the Coop is working on launching a stablecoin variable yield index, an NFT index, a diversified crypto index, a 0xPolygon index, a DeFi growth index, and more. These additional indices will attempt to meet customer demand for gaining on-chain exposure to unique products.

Issues & Uncertainty

Although Index Coop has a dominant position in the on-chain passive asset management market, it still has several issues. It has poor negotiating power with two of its “suppliers”, on-chain passive investing is likely too early, and there aren’t great methodologies for its indices yet.

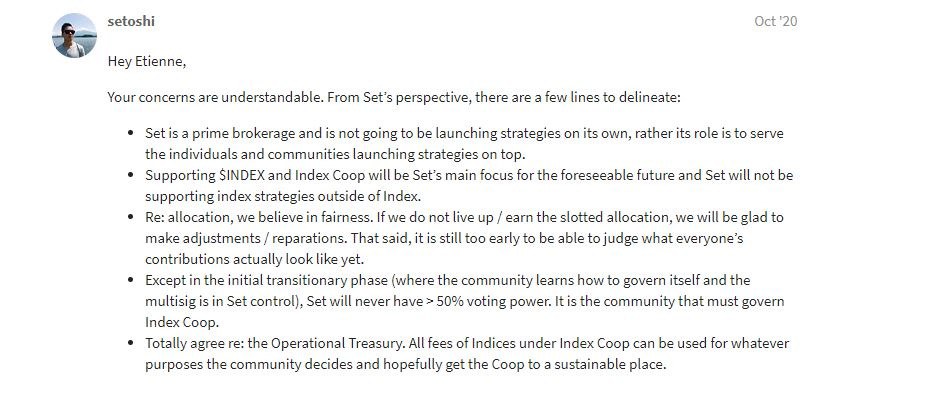

Index Coop has historically relied heavily on Defi Pulse and Set Labs for its index infrastructure and methodologies. Although this made sense during the early stages of the projects, Index is getting closer to profitability and is seeking autonomy.

The Autonomy Working Group was established in Q3 2021 and has worked on how to rely less heavily on its parents. Although this is good for the long-term viability of Index Coop, Set Labs and Defi Pulse are justifiably unhappy. DeFi Pulse gets a kickback on its indices that it manages for Index Coop, and it’s unclear which future indices will fall under DeFi Pulse’s domain.

Similarly, as Index Coop attempts to become more autonomous, Set Labs is subtly diversifying its revenue. Set Labs has several new customers that are direct competitors of Index Coop.

Set was committed to supporting Index Coop a year ago.

Now their loyalty is starting to sway.

Another issue is a question of “is the target market for passive crypto indices already on-chain?” Passive indices are meant to abstract away the decision-making process for prospective investors. On-chain indices will give investors access to collateralization and yield on their investments. Currently users of defi products are generally quite knowledgeable about crypto and it’s hard to believe that many of these “crypto natives” would want to take a passive approach to their investments. In a few years when transactions are cheaper due to scaling solutions and UIs are improved, we may start to see Index Coop’s target market start to emerge on-chain.

The last issue I’ll mention has to do with methodologies. It’s difficult to have an index methodology that performs well vs. the market over a long-time horizon. This is due to high operating leverage (requires scale), subjectivity in reweighting, and pace of development in crypto. Besides reaching a large enough AUM to compete on fees vs. traditional vehicles, there isn’t an obvious solution to underperformance.

Look at the DeFi Pulse Index. There are arguably 5 tokens in this set that are “dead”. I find it hard to believe that there’s an objective way to remove dying projects from the index quickly to stop underperformance. Some of these projects had reasonable enough operating metrics for a long time, but the fundamental aspects of their tokenomics/or business plans suggested there wasn’t going to be long term viability. Crypto is still too small (investable protocol list for indices is low) and there aren’t generally accepted accounting principles to normalize different project operating metrics yet.

Index Token

$INDEX is a governance token for the Index Coop. The value of governance is access to protocol cash flows and metagovernance over tokens in Index products.

Metagovernance: INDEX holders can vote on governance proposals for protocols like Aave and Compound because the Defi Pulse Index has those assets in its holdings. This power isn’t trivial either. INDEX has over 100,000 Aave votes and is able to create proposals for Aave. As Index AUM grows, metagovernance becomes more valuable. Index Coop has by far the most metagovernance powers of any passive asset management protocol.

Valuation

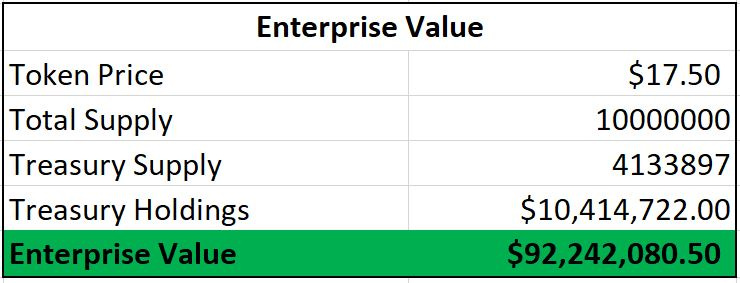

$INDEX has an “enterprise value” of $92 million and a fully diluted marketcap of $175 million.

Index Coop holds a large amount of its treasury in its native token. It also has several million dollars of stable coins and some allocations to each of its indices.

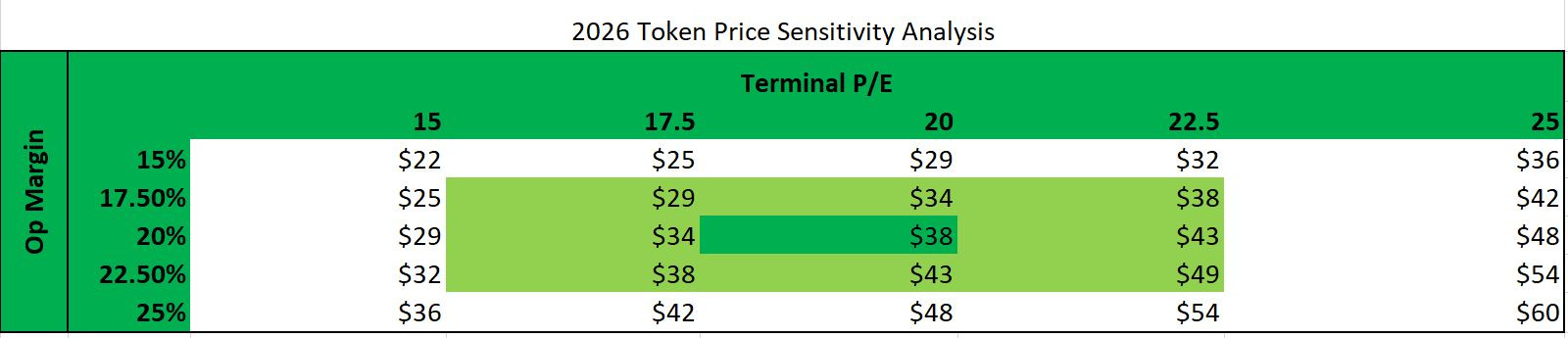

Speculating on $INDEX valuation requires an implicit bet on the future total marketcap of crypto. I created a reverse DCF to see what the market was assuming for Index Coop’s growth prospects.

I think that the market is coming around to the idea that streaming fee compression is unavoidable. A large institution that would consider investing in an index product could recreate the same product through Set Protocol and avoid paying fees. There’s added complexity with doing that, but it still suggests that Index Coop doesn’t have much pricing power. I assumed that the Coop will be able to collect 25 bps for streaming fees in the long term. The market is likely assuming that Index Coop will have roughly $22.5 billion TVL in 2026.

All things considered; I don’t think those growth assumptions are necessarily aggressive if we assume TVL partially grows from the crypto market cap increasing.

If we assume long term operating metrics with today’s revenues, $INDEX is trading at roughly a 356 normalized P/E.

If we assume that $INDEX succeeds to get ~$22.5 billion TVL in 2026, I’ve created a sensitivity analysis for gauging $INDEX price based on different operating margins and PE ratios.

Conclusion

Index Coop is the main player in the on-chain passive index market. It has a large total addressable market and continues to push out new products. I think that the price of $INDEX can increase significantly if the Coop can successfully create more defensibility for its streaming fees and can solve some of the issues addressed in the article.

As of now, I don’t feel comfortable holding $INDEX tokens and would rather wait for some of the problems to subside before taking a position.

$INDEX trades at a high multiple relative to my belief of it’s long term margins. I don’t have the confidence to assume consistently high growth at the moment until some of the issues I’ve discussed start to dissipate.

I’ll be watching for

Revenue diversification away from Defi Pulse controlled indices

More concrete details to be released discussing Set Labs and Index Coop’s relationship

New methodologies that can potentially outperform their benchmarks

Growing customer base

Product launches on layer 2s and sidechains

Better UI and onboarding for defi wallets

Index listings on tier 1 exchanges

Disclosure: I don’t own $INDEX tokens or any other tokens mentioned in this article.

Disclaimer

Nothing contained herein constitutes financial, legal, tax, or other advice. Noah makes no representation that the information and opinions expressed herein are accurate, complete, or current. The information contained herein is current as of the date hereof, but may become outdated or subsequently may change.

The mention of or reference to specific strategies or instruments in this presentation should not be interpreted as a recommendation or opinion that you should make any purchase or sale or participate in any transaction.